Media Summary: Unlock the secrets of financial risk management with Ryan O'Connell, CFA, FRM, as he dives deep into Code on github: Welcome to the fifth episode of my tutorial series on ... Hello Candidates, In this video we will be talking about the concept of

Programming Expected Shortfall Based On - Detailed Analysis & Overview

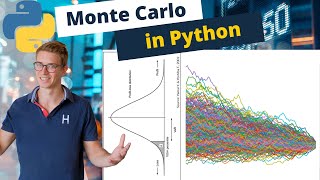

Unlock the secrets of financial risk management with Ryan O'Connell, CFA, FRM, as he dives deep into Code on github: Welcome to the fifth episode of my tutorial series on ... Hello Candidates, In this video we will be talking about the concept of ES is a complement to value at risk (VaR). ES is the average loss in the tail; i.e., the Designed for CFA and FRM Part 1 candidates, this video clearly and simply explains the Risk Management concepts of Value at ... Why did Credit Suisse and Silicon Valley Bank collapse overnight? It wasn't just "bad investments"—it was a failure of math and ...

Expected Tail Loss By Using Function in Python In today's video we follow on from the Monte Carlo Simulation of a Stock Portfolio in Python and calculate the value at risk (VaR) ... In this Video we willl understand all the key concepts about In this video, I'm going to show you exactly how we calculate How to address the limitations of value-at-risk? One of the most famous techniques used to measure In this short video from FRM Part 1 curriculum, we introduce this risk measure

Financial education for everyone Mastering Conditional Value-at-Risk (CVaR) / Check out our Full Suite of Market Risk courses online: