Media Summary: Autoregressive conditional hereroskedasticity ( Generalised autoregressive conditional hereroskedasticity (GARCH) is an extension over Master Quantitative Skills with Quant Guild* * Interactive Brokers for Algorithmic Trading* ...

Arch Model Volatility Persistence In - Detailed Analysis & Overview

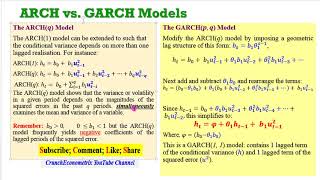

Autoregressive conditional hereroskedasticity ( Generalised autoregressive conditional hereroskedasticity (GARCH) is an extension over Master Quantitative Skills with Quant Guild* * Interactive Brokers for Algorithmic Trading* ... These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. MIT 18.S096 Topics in Mathematics with Applications in Finance, Fall 2013 View the complete course: ... In this video you will learn how to estimate a GARCH

Threshold GARCH (TGARCH) is an extension over GARCH models proposed by, among others, Jean-Michel Zakoian in 1994. In this lecture we explain the EGARCH (Exponential GARCH) Using monthly exchange-rate data, we use the "rugarch" package to estimate a GARCH(1,1) process off of an AR(1) mean ... Please pardon my gaffes. Referring to “ In this informative video, we'll introduce you to the basics of the In this time series tutorial, I will teach you how to estimate